The Dollar is Dead

When belief dies, fiat dies with it.

Let’s just hop right into it and start with my boldest claim of the summer:

By 2040, the U.S. dollar will no longer be the global reserve currency.

And maybe an even spicier take:

It might not even be the default unit of exchange for Americans back home.

Gasp. What did he say?! No more Hamiltons for morning Starbucks? No Benjamins for blackjack at Bally’s?! Say it ain’t so.

If you know me personally, you’ve probably heard me spitballing versions of this since we lit the dollar on fire during COVID.

But the last four months have crystallized something for me: this isn’t just some long arc of decline we’ll debate from our rocking chairs. It’s happening. It’s happening now. It will absolutely happen within our lifetime, and I expect likely in the next decade.

Before I throw down my 8-Mile-style rap battle against the greenback, I want to call out that there are many dissenters. Plenty of people, who are more credentialed than me on this topic, think I’m totally wrong. Over the last few years I’ve floated this theory in conversation with investment bankers, Fed economists, Treasury staffers, economic historians — all people with front-row seats to the fiscal drama, who in principle should know better.

Without fail, they give me a tight-lipped smirk that says: “cute theory, but the dollar’s not going anywhere”, citing the sheer volume of sovereign reserves denominated in USD, the dependence of the global financial system on T-Bills and long-dated treasuries, the lack of a legitimate competitor that can meet the demands of international trade and FX swaps.

They all say the same thing, and all cite the same facts and numbers. And that, right there, is exactly why the dollar will be no more.

This way of thinking belongs to the category of Dumb Rules™ — the kinds of beliefs that become institutional dogma long after their founding logic has withered. And I’d place “The dollar is irreplaceable” right at the top of that pile.

So let’s look at three facts that, taken together, tell a different story.

I. Markets Now Beat Policy

Let’s start on Liberation Day, April 2, 2025 (not to be confused with the day before, April Fools Day).

As an aside, “Liberation Day”, has to be one of my favorite Trumpisms — because it was, in fact, a kind of liberation. Not from tyranny or communism or anything drammatic — but from Common Knowledge. Namely, the post WWII belief that free trade is good, globalism is a rising tide that lifts all boats, and that Americans back home are better off using their fingers to scroll iPhone screens, than screw in the bolts near the power jack.

I digress.

When Trump announced sweeping tariffs (or really just gestured aggressively in their direction, see TACO), markets freaked out. The S&P dropped over 12%. And that made sense — tariffs should shift prices up, and price hikes should in principle suppress consumer demand. Revenues will drop, corporations will lay off employees to maintain operating margin, unemployment will spike.

Classic recession signal.

So what do markets normally do when a recession is incoming? The yield curve inverts. Institutional capital hides out in long-dated Treasuries. Bond yields fall with the expectation that the Fed will step in and make money cheap to restart the business cycle, incentivizing capex and job creation.

Except… they didn’t.

Instead, Treasury yields spiked.

This was the opposite of what happened in ’81, ’90, ’01, ’08, or even 2020. And it tells us something profound: financial markets no longer respond to expectations of monetary policy — they respond to whether dollars are a good store of value in the long run. And right now, expectations are simple:

The government will always spend more money, and the US will continue to recede away from its global leadership role.

How do you keep prices low with tariffs? Spend money.

How do you support bond markets? Spend money.

How do you follow through on campaign promises? Spend money.

How do you stimulate GDP? Spend money.

At the Federal Reserve, spending money doesn’t mean paying down your balance sheet. As the creator of the global reserve currency, the US pays our debts in the money we print — so spending money means printing more of it.

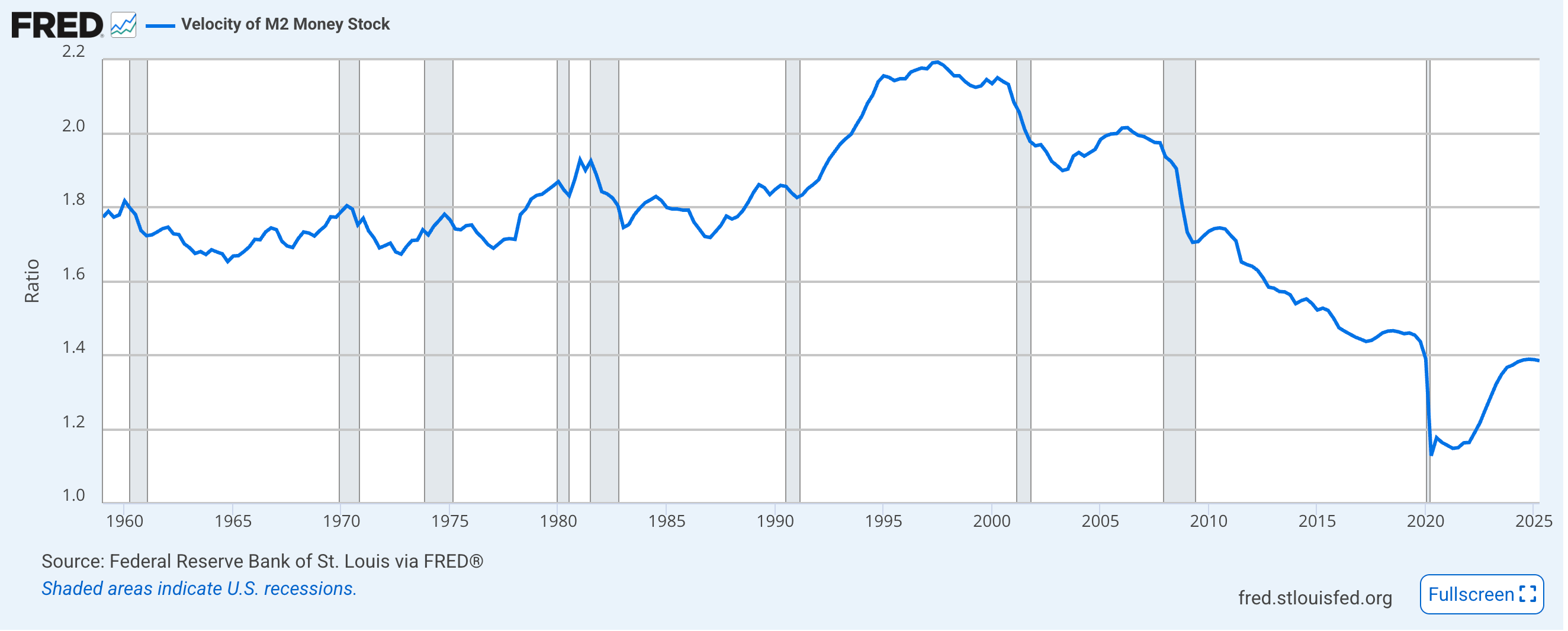

In the past 20 years, we’ve overdone it. Historically, the ratio of nominal GDP to the volume of US dollars (known as money velocity) held steady at about 2 — but since the Great Recession, we have printed freely to stabilize the credit markets, and that has led to a dramatic drop in money velocity:

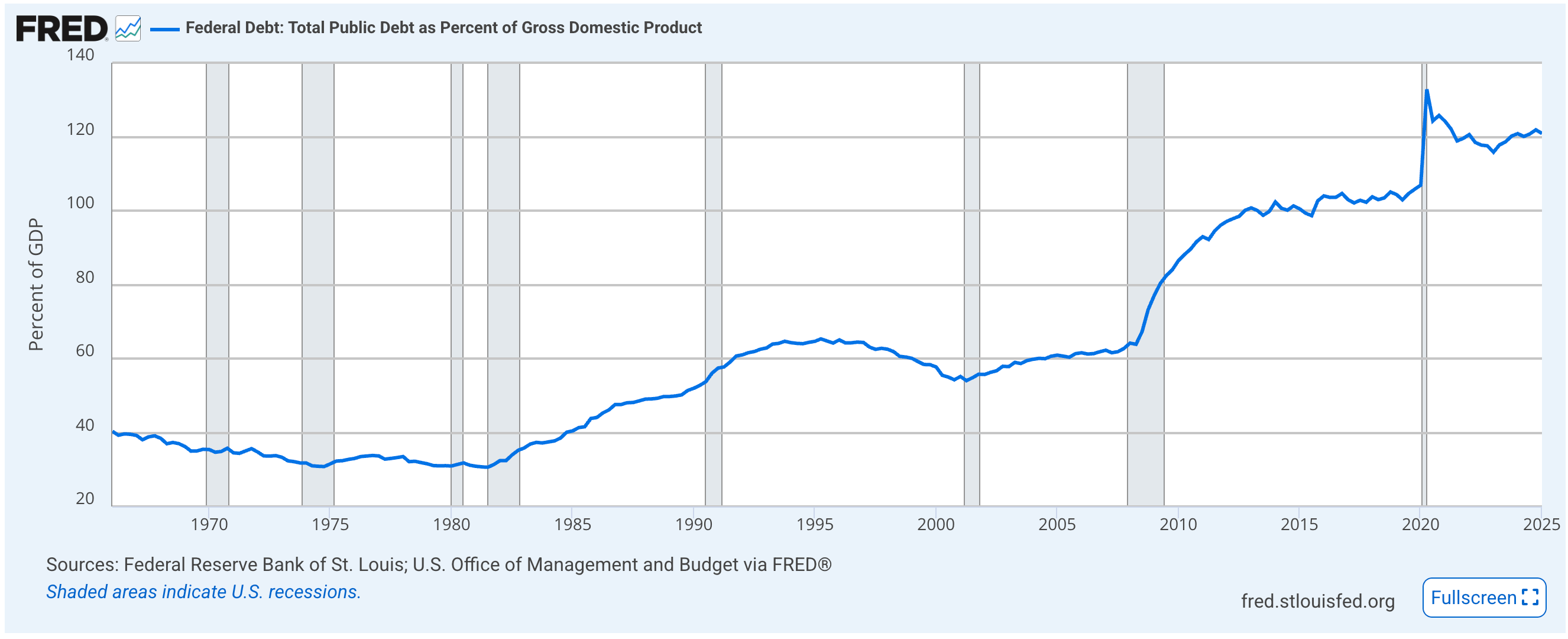

Meanwhile the debt to GDP continues to rise with every global crisis, far outpacing the growth of real GDP. The more debt you add that is rejected by global partners, the more the Fed will have to purchase with new money to support the US credit market.

This trend, an oversupply of money and an excess of dollar denominated debt, has been watched by the bond market for decades now — and this past spring, they said no more. Now the markets are calling the shots, not the Fed. And when markets start dictating monetary outcomes instead of central banks, you’re no longer in control — you’re just managing optics.

And the optics aren’t great. So here’s my first projection:

Projection 1: Long-dated bonds will remain high even if the Fed drops the overnight rate. If interest rates drop, there is so much M2 floating around that spending will accelerate suddenly and rapidly, leading to a spike in inflation above 5%. This will be immediately priced in by the bond market, and long term yields will spike in order to get a real return.

In short, we have already reached the point of no return - and I think the 10-year will continue to rise:

The bond market has commandeered the ship — and principled monetary policy is no longer in control. The days of an inverted yield curve are over.

The tail now wags the dog.

II. The Unseriousness of Our National Debt

These dynamics in the bond market are the first domino to fall, and they signal something the US Treasury Department already knew in the last administration. Take Janet Yellen’s last move as Treasury Sec, for example: she sold off mostly short-dated bonds even when interest rates were scraping the floor following COVID.

Seems insane, right? Why lock in short-term liabilities when long-term money was practically free after the pandemic?

Because Treasury saw the elephant in the room. As Janet shopped around bonds to anyone that would take a meeting — China, Japan, Europe — there was no appetite for 30 year U.S. bonds with interest rates under 2% when Debt-to-GDP was above 120% following COVID stimulus. The market wouldn’t touch them — even if we asked.

So it wasn’t worth asking — because again, at this point, Treasury and Fed are just managing optics. So instead of refinancing our liabilities at historic lows, we front-loaded the interest burden. Which means the window for monetary discretion — raising or lowering rates, modulating the money supply, nudging inflation — is effectively closed.

At this point, lowering rates would be seen as an inflationary signal, and the bond market will punish us in turn. Just ask Japan.

So we have a predicament - we can’t lower rates anymore without spiking long term yields - and we can’t hike rates without blowing up the budget with debt servicing payments. Why? Because the last time we hiked rates to save the dollar, we were in a completely different fiscal position.

Take a look at the Debt/GDP since the 60s,

and likewise the Fed Funds rate over the past 60 years:

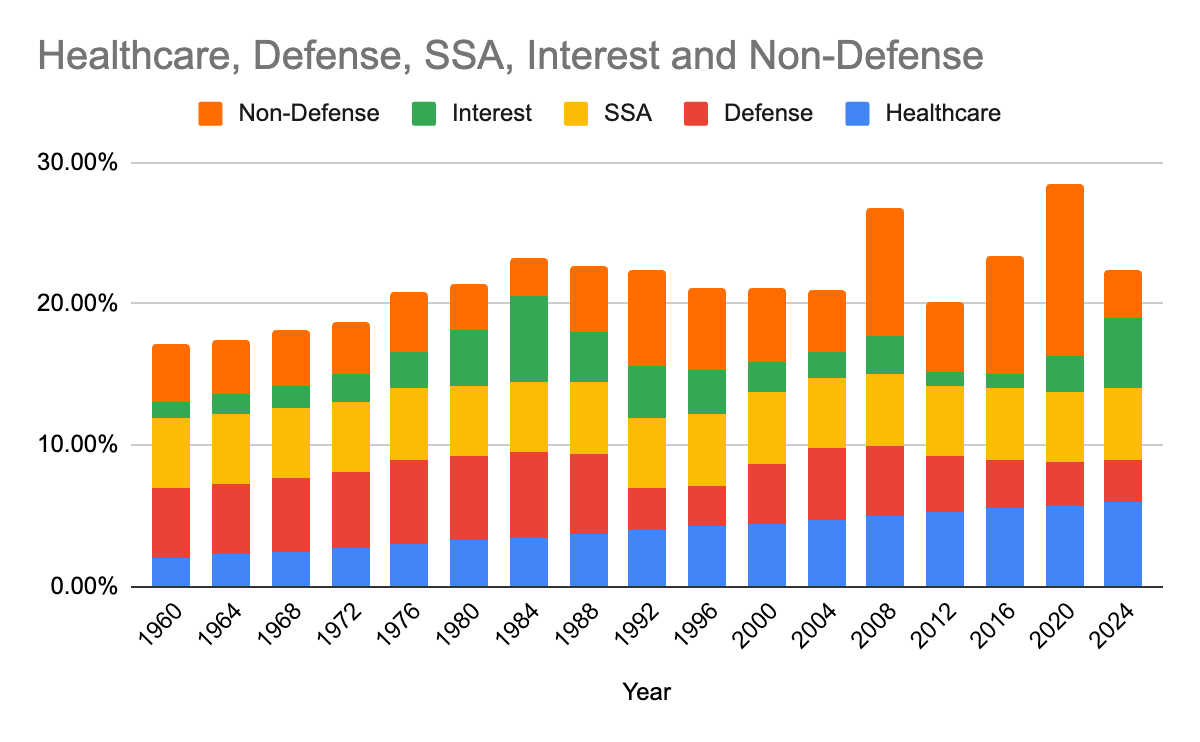

Multiply these two numbers together and you will roughly get the amount we pay each year (with some lag) in debt servicing out of our annual budget. To see what this means in practice, we can plot the percent of US GDP spent on the 5 main categories of our federal budget:

Social Security

Healthcare

Interest Payments

Defense Discretionary Spending

Non-Defense Discretionary Spending

The US brings in roughly 15-18% of GDP as tax revenue, and grows about 3% in real GDP. So when the spending is above that range, the Debt/GDP goes up, and when it’s below, it goes down.

In the plot above, we can see the portion of our spending that has gone to interest payments — with an important observation: as a percent of GDP, we pay the SAME in interest payments TODAY as in 1980 when the interest rate ballooned to 18%.

So, if we ever had an inflationary epoch like we saw in the 1980s, we would be unable to harden the dollar with interest rates — 12% interest rates today, would result in interest payments that make up 100% of our annual tax revenue. This would likely lead to a debt death spiral, and would spell the end of the dollar.

So Treasury and The Fed’s hands are tied - the dollar is currently squeezed by fiscal uncertainty.

That means the American institution that is left in control of the dollar’s fate by keeping spending (and thus the debt) under control is…. Congress.

LOL. Yikes.

This is where things get a little less spicy and I can just say what everyone else already knows:

Congress is inept and will continue to spend above our means because it is politically expedient to do so for the party with the purse strings that happens to be in power.

Indeed, there’s a long history of this. The political turbulence that we see in congress isn’t just unsettling — it’s expensive.

This is also true of the Executive branch: new administrations always spend more than those that have just been re-elected — pushing the obligation of fiscal responsibility onto the next guy. In fact since 1970, all increases in Debt to GDP have come in the first term of US presidents:

Fact 1: First-term presidents grow the nominal debt by ~13% per year.

Fact 2: Second-term presidents grow it by ~6% per year.

In other words, while governing is expensive, it’s manageable (nominal GDP has grown at 6% a year dating back to the 1950s) — but fulfilling campaign promises is reckless. And yes, I would consider Trump 47 a second round at a first-term presidency — and when viewed in those terms, the spending in the OBBB is par for the course.

This is nothing new.

Our political system encourages irresponsible spending every time power changes hands. The Bipartisan Infrastructure Law, the Inflation Reduction Act — massive trillion-dollar bills dropped in politically volatile environments. Because no one wants to be the adult in the room anymore and say “you know all those things I campaigned on? It turns out we can’t afford it”.

So this brings us to my second projection:

Projection 2: Election cycles for the next 20 years will remained deadlocked at a 50/50 toss up. The tie break will be given to whoever moderate and centrist voters hate the least — i.e. the new and unvetted candidate. As we oscillate back and forth between one four-year term after another, the new administration will do what they’ve done for 50 years — spend with abandon, only to get voted out before they had time to realize they represented The People, not The Party.

When no one wants to be the adult, the kids run the house - and kids don’t worry about paying down the mortgage.

III. The Politicization of the Fed

And sadly, the adults in the room are slowly getting cannibalized by the Lost Boys.

This, to me, is the final nail.

The Fed is the last American institution left with any pretense of independence. But in the past year, we’ve seen that too begin to crack. The Administration publicly criticizes the Fed’s decisions, which I will admit is not new (Reagan was a very vocal critic of Volcker’s Fed, and even suggested he would “go visit them in-person” like a mob boss — which at the time was unheard of).

However, what is new is fabricating grounds for a premature dismissal — with talk of firing Jerome Powell “for cause.” Indeed, we just saw the head of the Bureau of Labor Statistics pushed out for alleged political bias — on grounds that the very data that can inform the Federal Reserve committee was itself politically biased.

At this point, it doesn’t even matter if Powell is removed before the end of his term. The Overton Window has already been shifted and the spotlight is now squarely on the Fed as a political body rather than what it was designed to be — the institution that backed the US Dollar when everything else crumbled around it.

For a century, the Federal Reserve Chair was an untouchable position — only ever replaced when stepping down voluntarily. Going forward, every new administration will bring not just new fiscal policies, but entirely new monetary philosophies — unmoored from precedent, data, or stability — the Fed Chair will be seen like the Supreme Court as a political surrogate.

But unlike the Courts, Fed Chair appointments are not lifetime — but just 4 short years.

So this brings us to my final projection:

Projection 3: Powell will be the last multi-term Fed chair. After Trump breaks precedent and chooses not to reappoint him in 2026, the next chair will be replaced by a new admin in 2030, and again in 2034, and again in 2038, and so on.

As monetary policy itself becomes a proxy for executive overreach, we will see the world continue to dedollarize, and sell off bad debt denominated in USD. The Fed’s balance sheet will continue to fill up with T-Bills and empty promises, and at this point, the spell will be broken and the US Dollar will be seen for what it is:

Paper and Bits.

Volcker saved the dollar because he had 8 years to execute on a vision of monetary policy that was deeply unpopular. Reagan had the opportunity to stop the experiment, but didn’t. That was leadership. A strong and stable dollar hurts in the short term, but forces fiscal responsibility in the long term.

What Happens Next

Howard Lutnik, Scott Bessent, and Ray Dalio have all pitched different versions of how to save the dollar and preserve the country’s balance sheet - it’s usually some combination of AI-fueled growth and productivity, deleveraging away from public to private markets with austerity, and imposing a strict 3/3/3 growth/inflation/deficit spending plan.

As someone that has sold a bunch of LLM enabled software over the past 6 months, I don’t really buy the AI capex turning into huge productivity gains. Everything to date has just been chatbots with RAG and API calls. None of them are going to do my laundry or file my taxes.

And as far as austerity goes — see Section 2: the kids won’t pay the mortgage.

Others have looked more towards what a post-dollar world would look like: a gold-backed currency. A basket of commodities. A BRICS+ crypto-alternative. Bretton Woods 3.0.

Personally, I think all of these miss the mark. As the world trends towards protectionism and bilateral trade deals outside the WTO, a fragmented, multipolar system with regional reserves seems far more plausible.

But all of this is noise — and none of it matters.

The key thing is de-dollarization is coming. Slowly at first, then all at once. The dollar may still be used, yes — but its days of global primacy are numbered — and it’s purchasing power will drop by orders of magnitude (think buying a cup of coffee with 5 Benjamins, instead of 5 Washingtons)

It won’t be because China “won”. It won’t be because Bitcoin became the new religion. And it won’t be because some magical new financial system overtook us (there aren’t exactly any good alternatives).

It will be because we lost the plot.

The strength of the U.S. dollar has always been downstream from the strength of U.S. institutions — the Fed, the Treasury, the Census, the BLS, the Courts. The public belief that the system would self-correct — even when flawed — gave the dollar its legitimacy.

But when belief dies, fiat dies.

In Closing: A Funeral and a Forecast

I don’t write this as a gold bug. I’m not a crypto evangelist. I’m not even particularly critical of the current administration. Because whoever comes next will do the same: campaign on disruption, fund campaign promises with debt, attack the legitimacy of their predecessors, and in the process, the US Dollar will melt away in the fire.

I’m just a physicist that stumbled into business, who’s spent the last few years building tools, running models, and watching patterns — and every signal I see tells me the same thing:

The monetary system we built for the 20th century, won’t survive the political cycles of the 21st century.

The dollar won’t vanish overnight. But it will lose the thing that gave it power: belief in the long-term coherence of the American experiment.

So let this be a eulogy. Not for a country. Not for an economy. But for the last great institution still standing.

The Dollar is Dead. Long live whatever comes next.