Daily Brief: The FOMC & Perpetual Motion

Daily Brief: The FOMC & Perpetual Motion

Fed cuts rates by 50 bps! What happens now?

Yesterday Jerome Powell announced at the Federal Open Markets Committee (FOMC) meeting that the Fed would set interest rate targets for 4.75% - 5.00%, which is a 50 basis-points (bps, pronounced “bips”) drop from the current target of 5.25%-5.50%. This came as a major shock — even to some Fed employees!

Market moving events like this rarely happen during trading hours. So it’s actually amusing to see effect it had on the Russell 2000 index when it was announced at 2PM ET:

Lower interest rates make borrowing easier, which typically benefits small-cap companies still in the cash-burning phase of development (revenue-bearing but pre-profit). Hence the bump.

But what about the broader economy? Let’s break down in more detail what this means for inflation, unemployment and future interest rates going forward. To understand this in depth, we first have to break down the perpetual motion machine that is the business cycle.

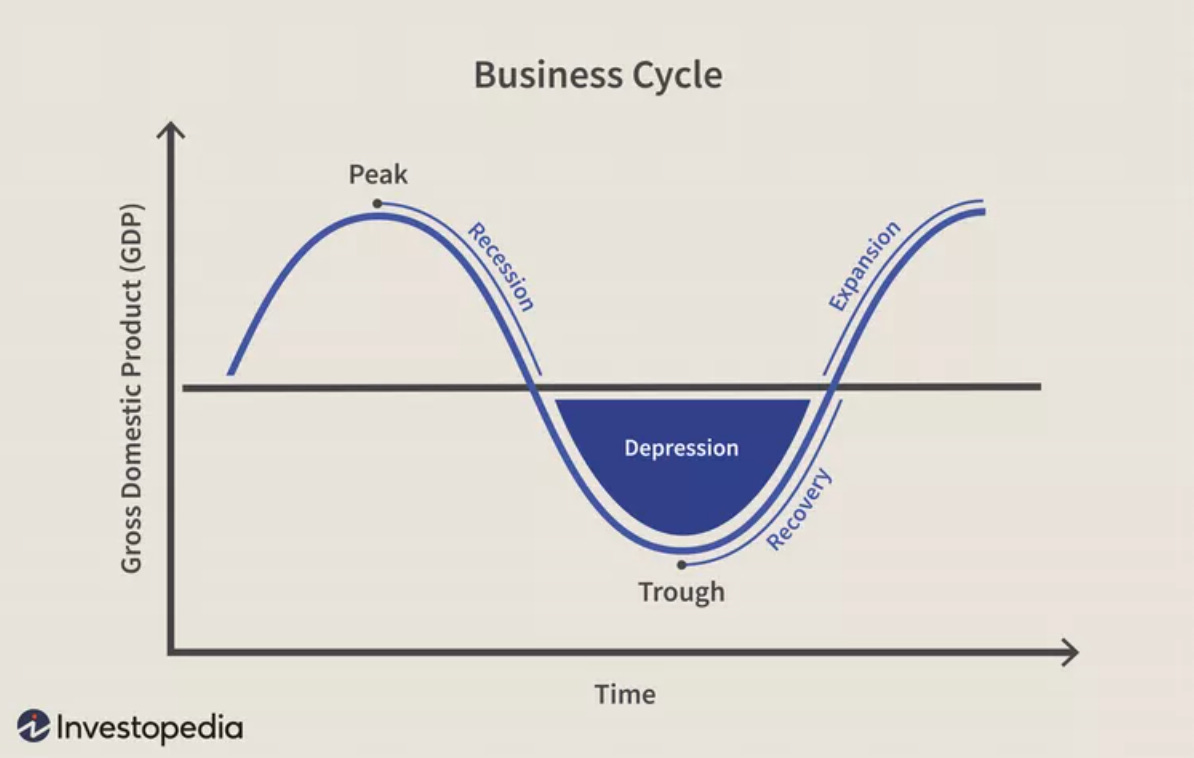

Short-Term Capital Markets Cycle

The short-term capital markets cycle, called the business cycle for short, is a natural ebb and flow in the growth and contraction of the US economy:

While the amplitude of this cycle (the height of the peak, and the depth of the trough) vary depending on other external factors, each phase represents a self reinforcing process that fuels the perpetual motion. Here’s how the business cycle goes on a step-by-step basis:

1-Up. Inflation leads to…

2-Up. Rate hikes leads to…

3-Up. Rising Unemployment leads to…

1-Down. Deflation leads to…

2-Down. Rate cuts leads to…

3-Down. Lowering Unemployment leads to…

1-Up. Inflation leads to…

2-Up. Rate hikes leads to…

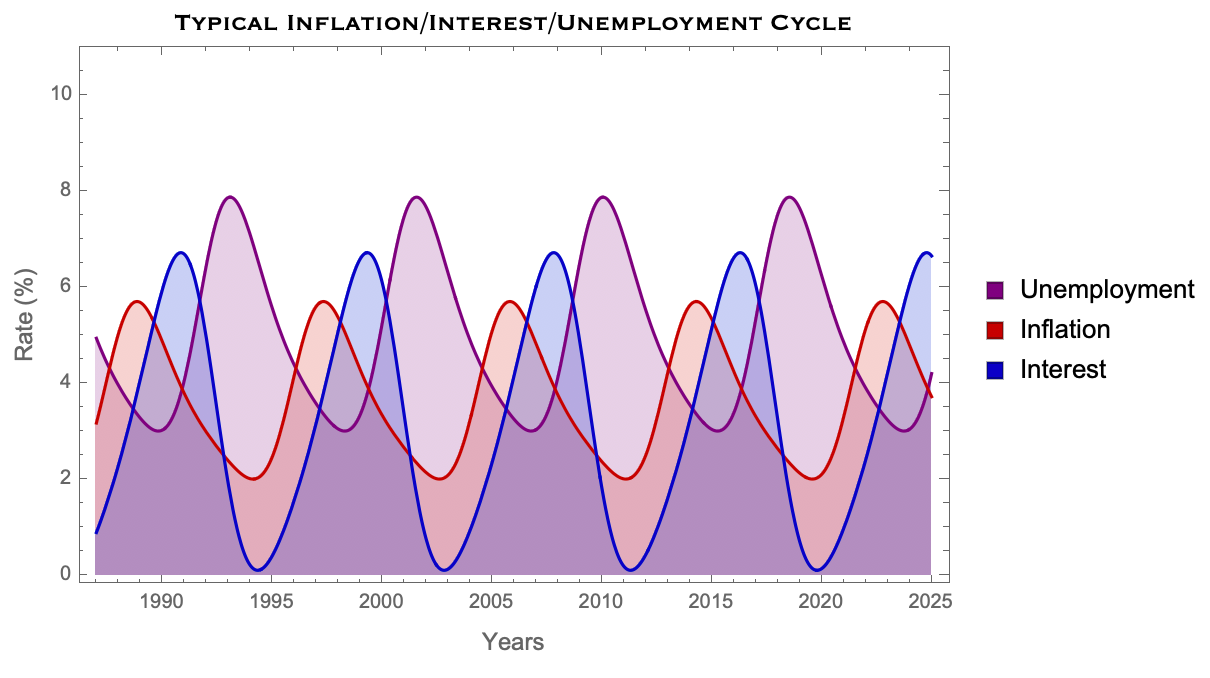

and so on. We can build a clearer picture of this using some simple trig functions, where the rise of one cycle leads to the next, and the decline then reinforces the next:

There are a few important features to keep in mind with this ideal model:

The cycle repeats itself on about a 7-9 year period.

Unemployment typically rises more quickly than it falls

Interest rates typically drops more quickly than it rises

Inflation typically rises more quickly than it falls

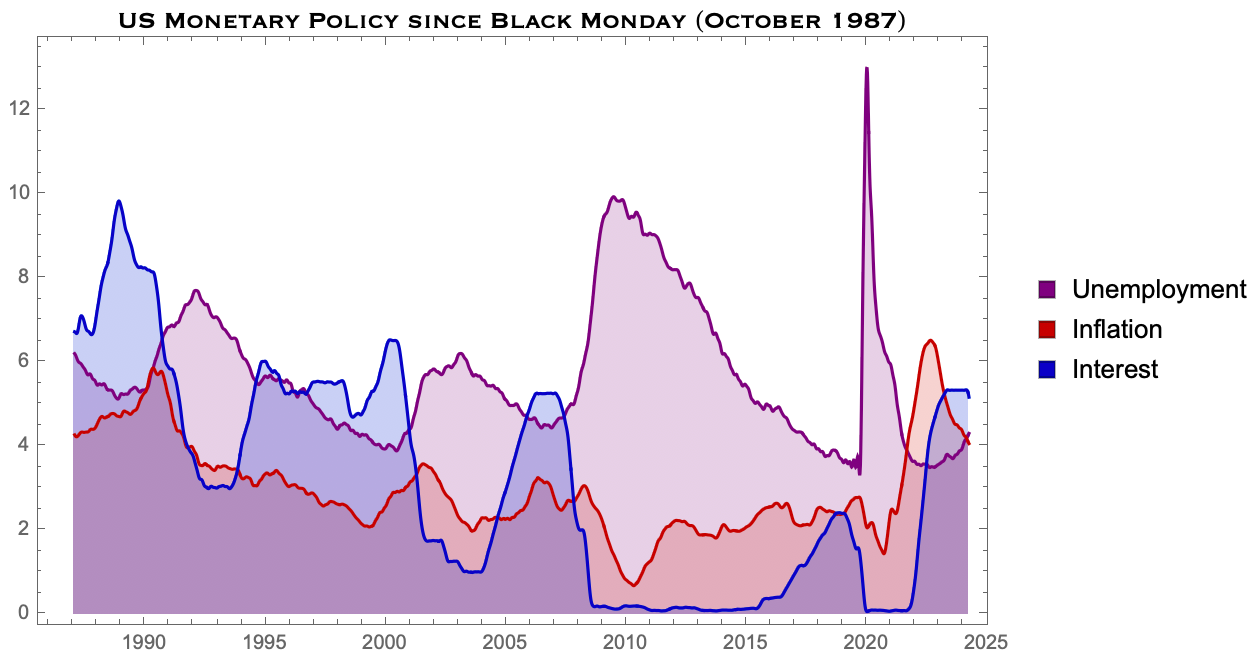

Obviously the real world is much less clean and subject to enumerable external events that are not tied to monetary policy (dotcom bubbles, junk mortgage bonds, global pandemics, etc.). But despite this, we can see essentially the same cycles at play in the real world data:

The Black Swan event of 2008 was so bad that it delayed the next cycle since there was a bunch of economic restructuring that needed to happen before restarting the cycle. Then COVID fast tracked the mini recession that we experienced in spring into fall of 2020.

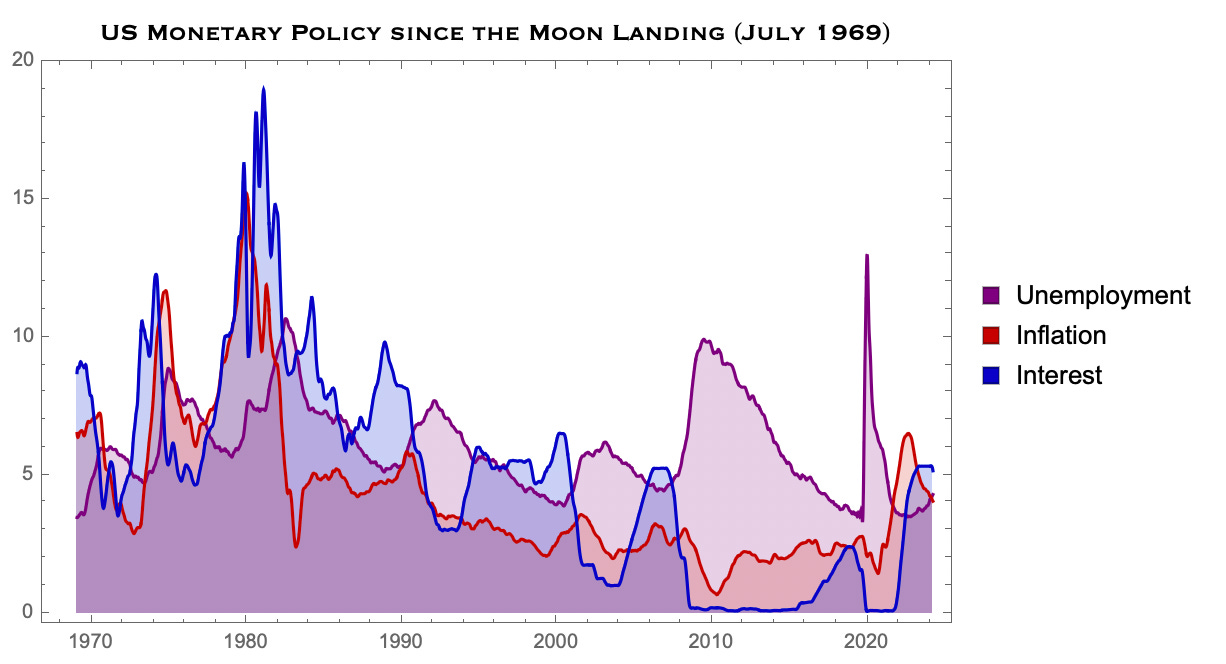

However, going back even further, we can see that the price stability for the US was much more uncertain. Post the Moon Landing in summer of 1969, the US experienced turbulent periods of hyper-inflation, commensurately high interest rates, and rampant unemployment (shown below):

A bunch happened during this tumultuous period (including decoupling from the Gold Standard) that I don’t have time to go into here. It’s just worth displaying in order to appreciate that recent history (past 35 years) was nothing compared to the price shocks of the mid 20th century1.

What does the Future hold?

Any Fed Chairman in Jerome’s position understands the ebbs and flows of the business cycle: so they’re just trying to minimize the amplitude of these peaks and troughs. The question is not IF unemployment will rise in the next 3 year, but rather, by how much will it rise?

Here are the options:

A soft landing would mean unemployment remains steady (4 - 4.5%)

A medium landing would like something like 1994 or 2001 (5 - 6%)

A hard landing would be anything resembling the pre-90s or 2008 (greater than 7%)

It’s worth noting that the last two times rates were cut 50bps (2000 & 2007), the market crashed shortly after. That being said, in the previous two 50bp rate cuts from peak, it had already been priced into the market.

Whereas this rate cut was a surprise to the capital markets. The price of treasury bonds last week suggested a 9-to-1 chance of a 25bps vs. 50bps rate cut. So it could be that the more aggressive strategy could protect the economy from the inevitable market downturn - and in that case, Jerome will have saved us all.

Only time will tell whether this surprise rate cut will save the economy from GDP contraction, while keeping inflation low, guaranteeing a soft landing.

In closing…

As the business cycle turns like a perpetual motion machine—constantly rising and falling with each shift in interest rates and unemployment—the inevitability of change becomes clear. Jerome Powell’s 0.50% cut signals that we are once again entering a phase where unemployment is set to rise. I’m personally pretty skeptical of all the analysts that think unemployment will hold steady between 4.4-4.6% over the next 3 years, just given what we’ve seen in the past 20 years.

Whether it’s a soft, medium, or hard landing, the cycle continues; reminding us that while we cannot stop the machine, we can understand its rhythm. The next few years will reveal where we this endless rotation will go, but one thing is certain: the motion never stops.

This is Math Meets Money.

Except 2008, that was pretty bad. Especially so if you lost your job and didn’t already own property outright.